Mera Ghar Mera Ashiana Scheme

The dream of owning a safe and contented home grows real with the Mera Ghar Mera Ashiana scheme. Through this programme at Bank of Punjab you ampule buy, build, reintroduce or refinance a house under practical terms. This guide explains everything from eligibility to leaflets, loan types, timelines and tips — after interpretation it you won’t need to search anywhere else.

| Program Name | Start Date | End Date | Amount/Assistance Provided | Method of Application |

|---|---|---|---|---|

| Mera Ghar Mera Ashiana (MGMA) | September 2025 (notification) | Ongoing | Subsidised home finance: Tier 1 up to PKR 2 million, Tier 2 up to PKR 3.5 million | Online + Branch (Bank of Punjab branch) |

What is Mera Ghar Mera Ashiana Scheme?

The Mera Ghar Mera Ashiana Scheme is a subsidised housing-finance inventiveness by the Administration of Pakistan together with banks (including Bank of Punjab) designed to endorse affordable cover. Through this arrangement you can:

- Purchase a ready house/flat

- Construct a house on your own plot

- Purchase a plot and then build the house.

It is for first-time homeowners and offers lower markup rates and longer tenures to make home-ownership achievable.

Why this scheme matters

In Pakistan many relations live in rented or unsuitable homes as market rates are tall. This arrangement goals to open the door to owning a home — “Apna Ghar, Apni Chhat” — under manageable terms, improving living values and contribution security for future generations.

Loan Products Under Bank of Punjab’s MGMA

Under the Bank of Punjab (and other banks) MGMA programme you will find several types of home finance:

- Home Purchase Loan – to buy a ready house or flat.

- Home Construction Loan – to build on your own plot.

- Home Improvement / Renovation Loan – to upgrade or expand an existing home.

- Refinance / Balance Transfer – transfer an existing home loan to Bank of Punjab under better terms.

These help you convert your income into an affordable monthly payment plan, turning your dream into reality.

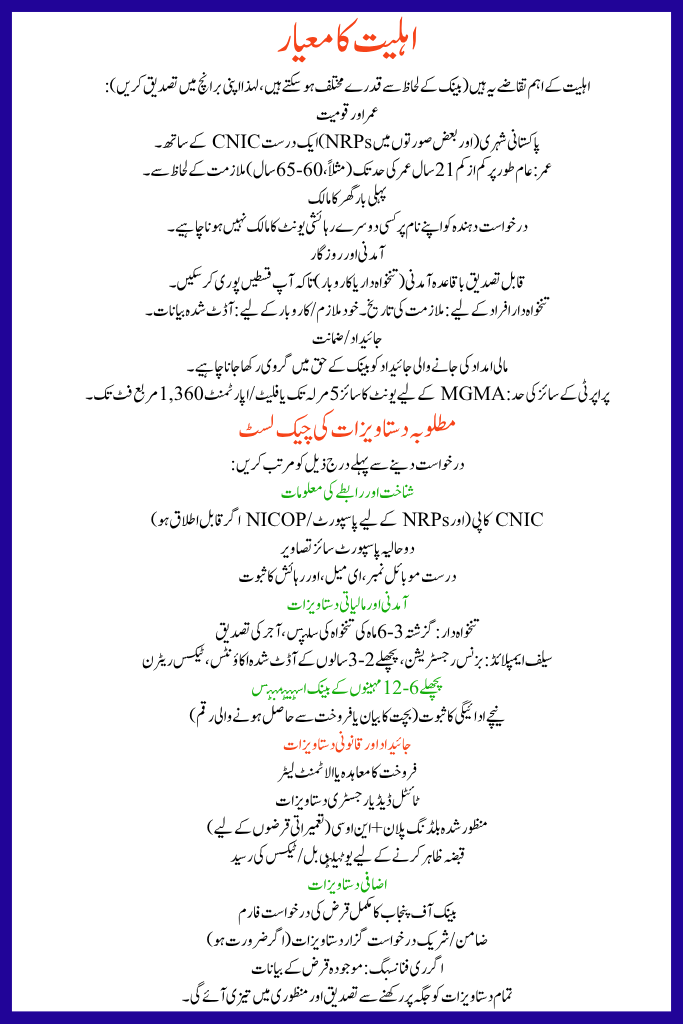

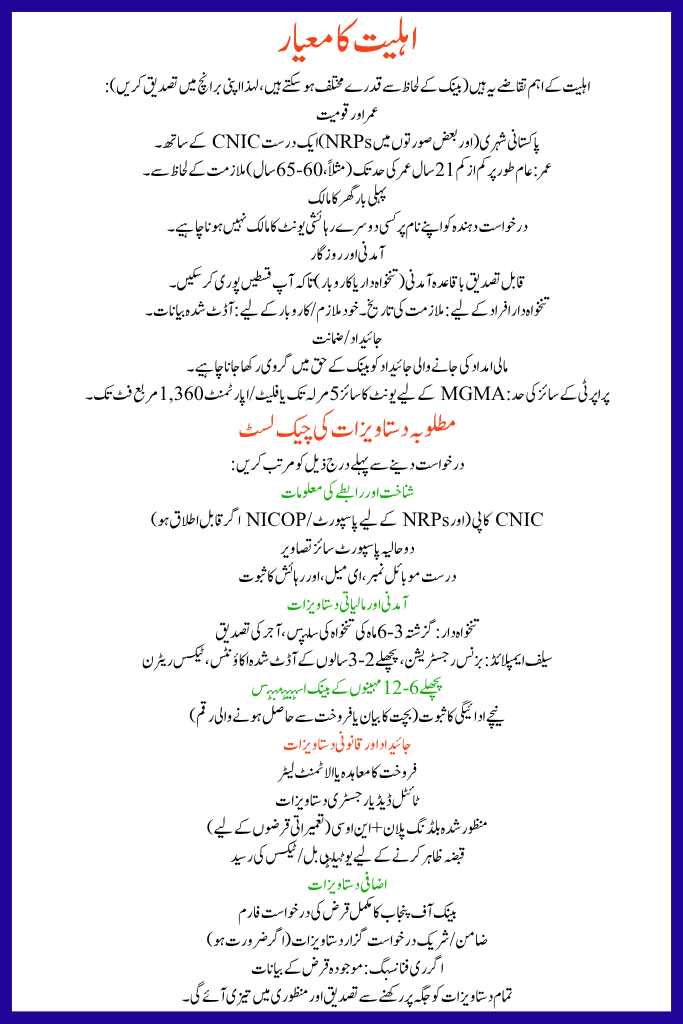

Eligibility Criteria for Mera Ghar Mera Ashiana Scheme

Here are key eligibility requirements (may vary slightly by bank, so confirm at your branch):

Age & Nationality

- Pakistani citizens (and in some cases NRPs) with a valid CNIC.

- Age: typically minimum 21 years up to age limit (e.g., 60-65 years) depending on employment.

First-time homeowner

- Applicant should not own any other residential unit in their name.

Income & Employment

- Verifiable regular income (salaried or business) so you can meet instalments.

- For salaried persons: employment history. For self-employed/business: audited statements.

Property / Collateral

- The property to be financed must be mortgaged in favour of the bank.

- Property size limits: for MGMA the unit size up to 5 Marla or flat/apartment up to 1,360 sq ft.

Required Documents Checklist

Compile the following before applying:

Identity & Contact Information

- CNIC copy (and passport/NICOP for NRPs if applicable)

- Two recent passport-size photographs

- Valid mobile number, email, and proof of residence

Income & Financial Documents

- Salaried: last 3-6 months salary slips, employer verification

- Self-employed: business registration, audited accounts of last 2-3 years, tax returns

- Bank statements of last 6-12 months

- Proof of down payment (savings statement or sale proceeds)

Property & Legal Documents

- Sale agreement or allotment letter

- Title deed or registry documents

- Approved building plan + NOC (for construction loans)

- Utility bill / tax receipt to show possession

Additional Documents

- Completed loan application form of Bank of Punjab

- Guarantor/co-applicant documents (if required)

- If refinancing: statements of existing loan

Having all documents in place will speed up verification and approval.

Application Process — Step by Step

Step 1 – Choose loan type

Decide: purchase, construct, improve, or refinance. Estimate how much you need, down payment, and tenure.

Step 2 – Initial Inquiry & Pre-Qualification

Visit your Bank of Punjab branch or contact through the bank’s home finance desk. Request pre-qualification to know roughly how much loan you can get.

Step 3 – Document Preparation

Gather all required documents listed earlier. Organise them neatly.

Step 4 – Submit Application

Fill out the “Mera Ghar Mera Ashiana” application form at your branch. Submit the documents and pay any processing fee (confirm if fee applies).

Step 5 – Verification & Valuation

Bank conducts verification of your employment/income/credit history. Property valuation and legal checks will be performed.

Step 6 – Offer Letter & Acceptance

If approved, you receive an offer letter showing loan amount, interest/markup, tenure, fees. Review carefully before acceptance.

Step 7 – Legal Documentation & Mortgage Registration

Sign loan agreement, register mortgage, complete stamp duty and legal formalities.

Step 8 – Disbursement

- For purchase: bank pays the seller.

- For construction: disbursement in stages after inspections.

EMIs begin according to the schedule.

Timeline for Approval & Disbursement

Here’s a general timeline (may vary by bank and applicant):

| Stage | Estimated Duration |

|---|---|

| Pre-qualification | 1-3 working days |

| Document preparation | 3-10 days |

| Credit & property checks | 2-4 weeks |

| Final legal steps & disbursement | 1-3 weeks |

Typical total time: 3-8 weeks from submission to disbursement.

Interest Rates, Fees & Tenure

Markup/Interest Rates

Under the national MGMA scheme (Government markup-subsidy) for affordable housing:

- Tier 1 (up to PKR 2 million): Customer fixed pricing ~ 5%.

- Tier 2 (above PKR 2 million up to PKR 3.5 million): ~ 8%.

Rates after initial subsidy period may shift to KIBOR + margin.

Tenure & Loan to Value (LTV)

- Maximum tenure up to 20 years (for MGMA scheme).

- LTV: Banks may finance up to 90% of property value under subsidy scheme.

Fees & Charges

Check for: processing fee, valuation fee, legal expenses, stamp duty, registration cost, any hidden charges. Under the government subsidy scheme some banks waive processing cost.

Example EMI (Illustrative)

If you take a loan of PKR 3,000,000 at ~ 14% for 20 years, your approximate EMI may be around PKR 39,000-43,000/month (depending on exact rate & tenure). Use bank’s EMI calculator for accurate figure.

Tips for a Successful Application

- Keep a clean credit history: pay bills, loans, credit card in time.

- Provide complete and accurate documents: missing items slow you down.

- A higher down payment helps reduce risk and improve approval.

- Consider a co-applicant with stable income if your income is modest.

- Ensure the property title is clear and free of legal issues.

- Be honest about any previous credit problems and provide explanation.

FAQs About Mera Ghar Mera Ashiana Scheme

Can NRPs apply?

Yes, Non-Resident Pakistanis can apply under certain conditions (with additional documentation).

Is the government providing subsidy under this scheme?

Yes — under the national MGMA markup-subsidy scheme the government provides subsidised rates for eligible applicants.

What if I miss an EMI?

Missing EMIs may lead to penalties, affect your credit rating, and risk foreclosure. Contact the bank soon if you face difficulty.

Can I repay the loan early?

Yes you can, but check the offer letter for any pre-payment charges. Under subsidy scheme some banks waive prepayment penalty.

Final Checklist Before Submission

- Completed application form for Bank of Punjab’s MGMA scheme

- Valid CNIC (and passport if applicable) + photographs

- 6-12 months bank statements

- Salary slips or audited business financials

- Property sale/title documents or plot ownership & approved building plan (for construction)

- Proof of down-payment

- Co-applicant/guarantor documentation if needed

Conclusion

The Mera Ghar Mera Ashiana scheme by the Set of Punjab (in partnership with the Organization’s subsidised housing finance initiative) offers an excellent chance for home-ownership. With proper groundwork, full certification and sympathetic of the process you can turn your dream of “Mera Ghar” and “Meri Chhat” into realism. Visit your adjacent Bank of Punjab division, ask for the MGMA product, make your flyers and apply. With the precise method, your own home is inside reach.

Related Posts